Cory Doctorow's linkblog · @pluralistic

40291 followers · 38187 posts · Server mamot.frAs #AdamLevitin put it on #CreditSlips:

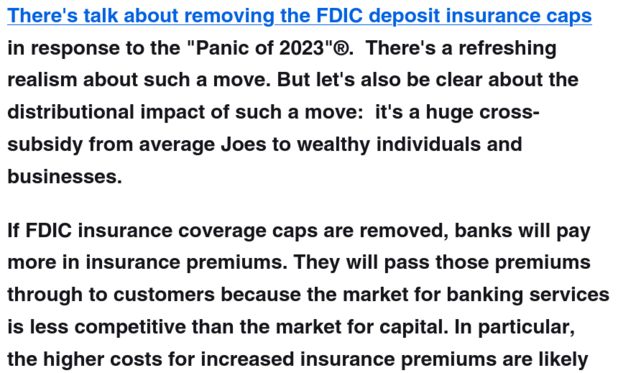

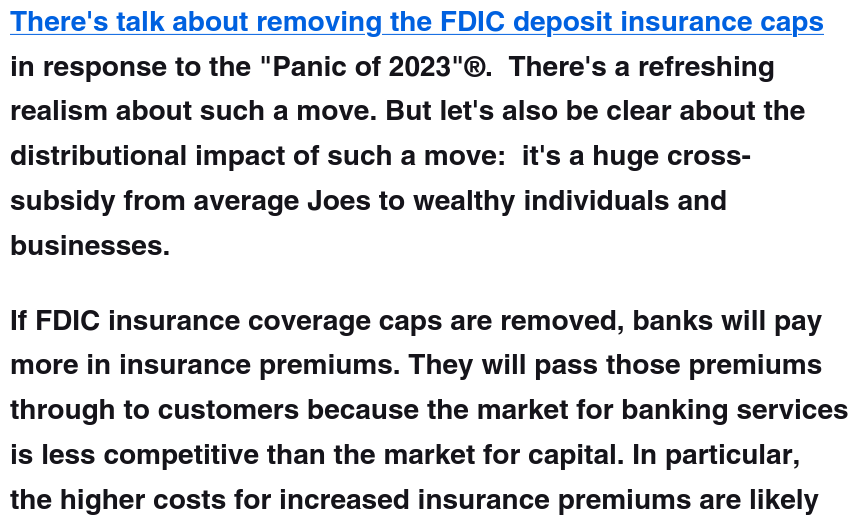

> They will pass those premiums through to customers because the market for banking services is less competitive than the market for capital. In particular, the higher costs for increased insurance premiums are likely to flow to the least price-sensitive and most “sticky” customers: less wealthy individuals. So average Joes are going to be facing things like higher account fees or lower APYs, without gaining any benefit.

6/

Cory Doctorow's linkblog · @pluralistic

39875 followers · 37259 posts · Server mamot.frWriting for #CreditSlips, the #FinanceLaw scholar #AdamLevitin admits to feeling a bit of schadenfreude in that moment. The "blue collar" law scholars in "grubby" banking and money fields have always treated the conlaw set as "slightly clueless toffs":

As a field, conlaw fiercely resists the idea that their field is "largely a battle of normative opinions, without any quasi-objective touchstone or clearly right or wrong answers."

2/

#creditslips #financelaw #adamlevitin

Cory Doctorow's linkblog · @pluralistic

39545 followers · 37053 posts · Server mamot.fr

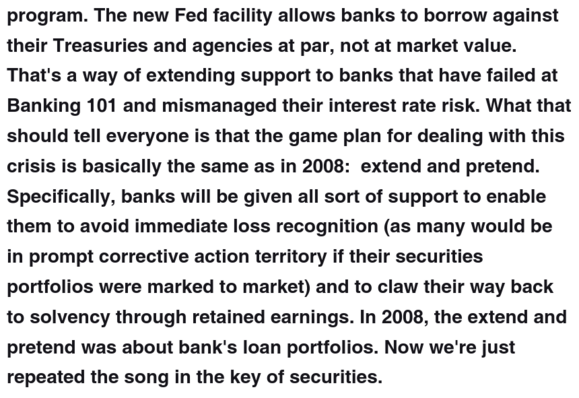

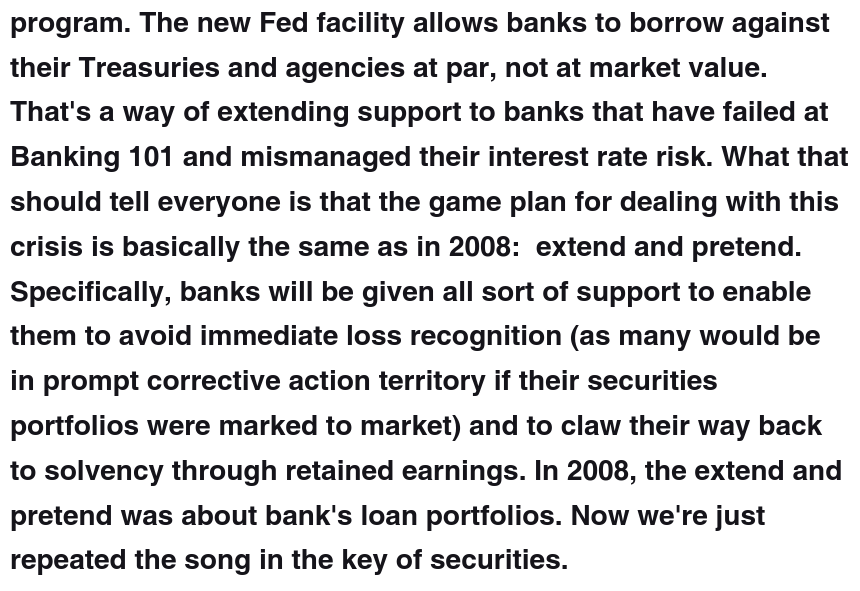

The #BankTermFundingProgram is a zombie-bank life-support program

Adam Levitin at #CreditSlips

https://www.creditslips.org/creditslips/2023/03/the-financial-regulatory-credibility-problem.html

#banktermfundingprogram #creditslips

Cory Doctorow's linkblog · @pluralistic

39545 followers · 37052 posts · Server mamot.fr

{kind=link}

{kind=link}

Lifting FDIC insurance caps is a way to get average people to subsidize billionaires - FDIC insurance costs are always passed onto everyday customers.

Adam Levitin on #CreditSlips